Responsible investment: How can the investment decisions of institutional investors improve their stakeholder impact?

In one way or another, all of us are beneficiaries of past investment. This highlights the responsibility of investors to optimise returns in a way that protects the progress and prosperity of both present and future generations. In boardrooms and universities across the globe, this has led to a growing discourse about responsible investment.

Why is responsible investment important for South Africa?

In one way or another, all of us are beneficiaries of past investment. This highlights the responsibility of investors to optimise returns in a way that protects the progress and prosperity of both present and future generations. In boardrooms and universities across the globe, this has led to a growing discourse about responsible investment.

This puts the spotlight on those people making the investment decisions – institutional investors. These ‘professional’ investors, as agents of other people’s money, have come to dominate investment holdings globally. They are mandated to manage the majority of assets, which translates into considerable power to influence decision-making in the companies in which they invest.

Traditionally, the message to institutional investors was: “Maximise risk-adjusted returns as much as you can. Don’t worry too much about the environmental and social impact of the investments.” Now there is a new narrative.

The World Bank identifies South Africa as having one of the highest ratios of inequality of all countries in the world. The legacy of the country’s colonial history, coupled with the global repercussions of financial crises and company collapses, has raised questions about the roles and responsibilities of institutional investors.

All over the world, this has led to the approval of new laws and the adoption of codes of corporate governance by civil society and increasingly by the private and public sectors. For more than a decade, we have seen ‘responsible’ investment principles, policies and practices emerging globally that integrate environmental, social and governance (ESG) criteria in investment decision-making.

The legacy of the country’s colonial history, coupled with the global repercussions of financial crises and company collapses, has raised questions about the roles and responsibilities of institutional investors.

As early as the 1960s, research on corporate executives in the US showed that over 80% of them felt that acting in the interests of shareholders alone was unethical. This led to the rise of stakeholder management, corporate social responsibility and corporate governance founded on principles that enable decision-makers to adopt a ‘stewardship’-orientated mind set.

Despite progress in policy and practice, research has found that barriers to the growth of responsible investment in South Africa outweigh the drivers and enablers of this investment philosophy. What’s more, there appears to be lack of commitment among local institutional investors to really embrace responsible investment.

To better understand the connection between institutional investors and the impact of their investment decisions, we need to take a closer look at the factors influencing the decision-making processes of South African institutional investors towards responsible investment (RI) – which is exactly what this study set out to do.

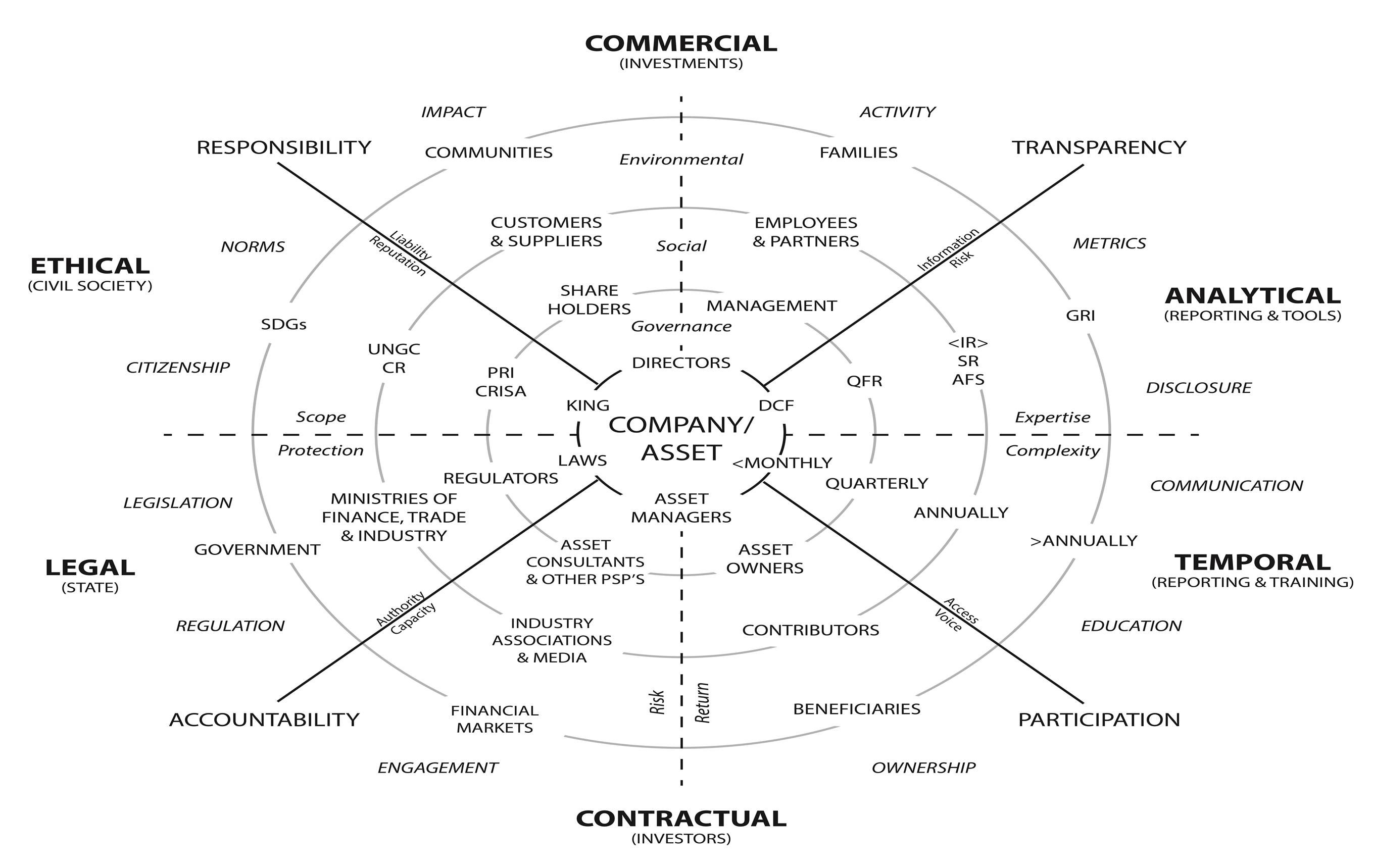

After reviewing current research on the topic and conducting a pilot study, the researcher interviewed 25 senior decision-makers working in the field of institutional investments. This led to the design of a framework that offers an integrated view of the factors influencing investment decision-making towards responsible investment.

The overall aim was to provide a tool that would help to offer a stakeholder-driven view of the investment value chain in order to improve RI policy and practice. The framework recommends mutual accountability in the investment value chain to optimise stakeholder salience, improve accountability, guide engagement and promote participation in the investment decision-making process. Another aim of this tool was to help address the inertia and inconsistency in the entrenchment of RI philosophy, policy and practice among local institutional investors.

Understanding the institutional investment value chain

Institutional investors, as opposed to individual investors, are financial institutions that invest vast capital into financial instruments on behalf of other institutions or the aggregated funds (like pension funds) of individual investors.

Institutional investors are key drivers and enablers of the global financial system due to the volume of assets under their management. Through their concentration of ownership, they have the ability to exert both internal and external influence through their activities. What’s more, they have the potential to influence external decision-making on financial and non-financial performance. They do this among other things by providing market signals whenever they sell, hold and buy more stock in a company.

To understand the complexity of the factors influencing the decision-making process of institutional investors towards responsible investment, it helps to see the institutional investment process from a value chain perspective. This investment value chain includes:

- Asset owners (AOs): This includes pension funds, provident funds, retirement funds, endowment funds, life insurance companies, banks, companies and non-profit organisations that invest pooled funds into various financial instruments.

- Asset managers (AMs): Asset managers have the delegated responsibility to invest capital into financial instruments and to manage those assets. Asset managers are appointed by asset owners.

- Professional service providers (PSPs): This includes asset consultants, research providers and investment advisors, accountants, lawyers and administrators.

- Network supporters (NSs): This includes industry associations, trade unions, regulators, academic institutions, special-interest groups, the state apparatus and other civil society bodies that have influence over a process, practice or participants involved in the institutional investment value chain.

The relationships between the stakeholders in this value chain are non-linear. Instead, the relationships represent a virtuous value chain – with each factor influencing the flow of value and information among the stakeholders in the business system all the time.

The flow of value – not just monetary value – between a business, its customers, partners (i.e. suppliers, vendors and distribution channels), employees, investors and competitors leads to interdependent value creation between parties. These relationships are influenced by external factors such as market conditions, environmental and community considerations as well as the legal and ethical regulations and norms applied by government and society. Various studies have confirmed that this sharing of information and knowledge helps to strengthen chains of accountability and knowledge when it comes to investment decisions.

Institutional investors are key drivers and enablers of the global financial system due to the volume of assets under their management.

The call for more responsible investment

When making investment decisions, institutional investors have a duty of care towards the functioning economy as a whole as well as to the individual companies in their portfolios considering how integrated company activities are on the social and environmental risks prevalent in the economies in which they operate. This has led to a call for more responsible investment and the emergence of normative frameworks and global initiatives that encourage such investment practices, especially after the global financial crisis of 2008.

Today, various global frameworks and collective initiatives encourage investment practices that promote the inclusion of ESG and ethical considerations into decision-making processes and company reporting. Examples include the United Nations’ Global Compact (UNGC), the UN’s Principles for Responsible Investment (PRI), the Carbon Disclosure Project (CDP) and Integrated Reporting. In South Africa, we have the King Codes of Corporate Governance, the Code for Responsible Investing in South Africa (CRISA) and the PRI.

One initiative that has gained global traction is the Principles for Responsible Investment (PRI). This code was born out of the United Nations Environment Programme Finance Initiative (UNEP FI). Since inception in 2006 to April 2018, the PRI grew to over 1 961 signatories with collective assets under management of over USD81,7 trillion. The UNPRI claims that 94% of its signatories have a responsible investment policy in place, with 71% requiring ESG reporting from their investments. This finding suggests that the principles do serve a purpose. However, their importance does not necessarily encourage organisations to become signatories.

Since the introduction of these frameworks, support for RI has been growing all over the world. What’s more, ESG considerations are increasingly applied in the decision-making of institutional investors in South Africa. And yet, research shows that local institutional investors lack the commitment to fully embrace the principles of responsible investment.

What then needs to change in the institutional investment landscape in South Africa for responsible investment to flourish?

The impact of institutional investment decisions

Investors increasingly want to know where their capital will be invested without necessarily sacrificing financial returns.

Responsible investment (RI) is an investment philosophy that transcends financial boundaries to recognise the impact of environmental, social and governance (ESG) criteria on investments and decision-making. It focuses on long-term investment, a broad-based consideration of investment criteria, ESG criteria in particular, and expectations of returns beyond purely financial metrics.

From an investment perspective, the history of South Africa suggests that decisions made by investors have significant social and environmental impact on the people and places where their capital is invested. Through their mandates, institutional investors assume a contractual responsibility to generate returns for their clients who are the contributors of the capital about which investment decisions are made. Institutional investors therefore need to make decisions about the allocation of vast amounts of capital. This puts them in a powerful position.

Investors increasingly want to know where their capital will be invested without necessarily sacrificing financial returns.

What should these institutional investors take into account when they make investment decisions?

Investment decision-making is a complex process

This study was undertaken to answer a question: What aspects of South African institutional investors’ decision-making process need to change for responsible investing to become the philosophy that guides their investment decisions?

In essence, the study wanted to better understand the connections between stakeholders in the investment value chain and, in turn, assess the effectiveness of RI principles and practice to achieve their promise.

Investors use various theories and tools to help them with decision making. These models largely employ quantitative methods to guide choices towards investments and instruments to achieve risk-adjusted returns for investors. Yet, the systemic nature of the relationships between decision-making, institutional investors and responsible investment is complex and unpredictable.

To complicate matters, transparency regarding the institutional investment decision-making process is affected by shareholder activism and investor literacy:

- Shareholder activism: Shareholder activists are institutional and individual investors who use their equity stake in a company to hold managers accountable for their actions. In South Africa, shareholder activism is on the increase although there is still much inertia and apathy when it comes to companies taking action.

- Individual investor literacy: Various initiatives are currently addressing the systemic challenge of financial literacy among institutional investors.

Who has power in the system?

The prevalence and influence of power dynamics in the decision-making process needs to be acknowledged. This includes the following:

- The stakeholder’s voice: The more power a stakeholder has in the value chain, the more salience that stakeholder has in the eyes of a firm against which it has a claim. In the context of institutional investment, such a firm could be an asset owner, asset manager, service provider or investee company. This shifting agency is known as the institutional investor’s ‘voice’ which is used to negotiate its priorities and interests within the stakeholder system. The institutionalisation of responsible investment – fuelled by the urgency to respond to ESG risks, accountability and the need for active ownership – is an example of how a stakeholder group can shift its agency, develop authority and create change. For example, Regulation 28 of the Pension Fund Act requires all pension fund trustees to ensure that pension fund assets are managed in line with ESG principles.

- The size of the stakeholder: Some of the largest institutional investors in the world and in South Africa (i.e. Government Employees Pension Fund – GEPF) are public sector institutions. Although some influential investors, such as the GEPF, are actively encouraging responsible investment, there appears to be a lack of commitment in this regard, even among PRI and CRISA signatories.

- Non-decisions: The power that institutional investors may have to influence a decision or outcome is not necessarily observed in their explicit participation in the decision-making process. They may also obstruct decision-making through their ‘non-decisions’. This subversive form of power also needs to be considered when evaluating the behaviour and motivation of the stakeholders involved in institutional investment decisions.

- Hard power and soft power: “Hard power” in decision-making refers to the use or threat of force to achieve an outcome, while “soft power” refers to the use of features like culture, value and policies that influence the behaviour of others without coercion. “Smart power” refers to the ability to draw on both approaches.

- Groupthink: The invisible power of groupthink needs to be taken into account, as this can lead to the ‘herding’ of decision-makers towards conventional decision-making processes.

- Incentives: Incentive systems have the power to reinforce behaviour. Investment incentives are often driven by short-term horizons, despite the underlying premise of RI seeking sustainable returns in the long-term.

In South Africa, shareholder activism is on the increase although there is still much inertia and apathy when it comes to taking action.

A conceptual framework for investment decisions that incorporate responsible investing

One of the outcomes of this study is a framework that takes into account all the stakeholder groups, as well as the ethical and analytical factors that can influence decision-makers or contribute to the investment decision-making process, integrating ESG criteria.

First, a pilot study was undertaken, followed by the main study which included interviews with 25 senior decision-makers in the field of institutional investment. The outcome of this is the framework represented below.

In practice, the conceptual framework proposes that ESG integration into the decision-making process connects market participants in the investment value chain, the respective behavioural dimensions of investors and the companies in which they invest, and the factors that drive the inputs and outputs of each dimension. The mapping of the factors across ESG domains and horizons suggests an interconnected, interdependent relational system. As an output, the mapping process offers a novel conceptual framework that could be used a diagnostic tool to assist institutional and individual investment decision-makers seeking to implement a stakeholder-orientated, more ‘responsible’ approach to their investments.

What else did the study find?

There was evidence of progress in the application of responsible investment principles and practice when comparing the perspectives of the interviewees from the pilot and main studies. This is what the study found:

The influence of power dynamics in the decision-making process needs to be acknowledged.

RI is not a fund or a signature, it’s an investment philosophy. There was little improvement in the number of South African PRI signatories over the study period. Although this statistic might indicate that RI is losing ground, feedback from participants suggest the opposite. The main study’s participants showed far more acceptance of the concept of ESG and its integration into investment decision-making. Even asset owners who did not know that much about PRI and CRISA agreed that ESG factors should be considered in investment decisions.

Reputation, not just performance, influences investor practice. During both the pilot and main phases of the research, there were complaints about certain PRI signatories’ non-compliance with reporting requirements. The researcher also noted that the interviewees, in their personal and professional capacity, ascribed a significant amount of value to their reputation. The preservation of reputation therefore provides an important motivator to influence invest decisions towards RI.

Professional investors are unaware of their governance liabilities. Financial service providers in South Africa are regulated in their individual and institutional capacities through legislation such as the Financial Advisory and Intermediary Services Act (FAIS), consumer protection laws and market conduct requirements as Treat Customers Fairly. Listed companies are expected to apply corporate governance frameworks to their operations. Failure to comply could lead to penalties, criminal and/or civil charges, imprisonment and/or the removal of licences to operate. Surprisingly, participants in the main study showed a limited understanding of the risks and liabilities associated with their responsibilities as investment decision-makers.

Trustees of pension funds appear to support short-termism. Asset owners in both the pilot and main studies had a clear understanding of their fiduciary roles and responsibilities but they were not very aware of RI principles and practice. Their main concern was the financial performance of their funds as they delegated the performance requirements of the funds to asset managers mediated through mandates and professional service providers like asset consultants. The performance of their funds was assessed quarterly, with only a three-year investment horizon applied to most asset managers’ performance measures. Asset owners interviewed in this study relied on peer benchmarks to compare performance, using the threat of switching their business to alternative asset managers should certain performance expectations not be met. Considering that asset owners oversee contributors and beneficiaries over generational thresholds, it was interesting to note that none of them applied long-term planning scenarios beyond a 10-year time horizon. This apparent lack of generational thinking supports their short-term approach to investment.

Public sector activity suggests ‘lender-of-last-resort’ role. In contrast to the role understood by private sector institutional investors, public sector participants in both the pilot and main studies seemed to assume responsibilities beyond the interests of their contributors and beneficiaries in the fulfilment of political, social and macroeconomic interests. Examples were shared of interventions and engagements with investee companies to stabilise markets, save jobs and promote the policies of the government. Interviewees recognised that, due to their size, they have the power to influence investment systems and therefore they aimed to act responsibly. During the study period they have taken action to avert the closure of assets, playing the role of lender of last resort. Due to their alignment with national government and the requirement for government officials to act as trustees and board members, there is an inherent conflict. In the pursuit of national interests, public sector asset owners and asset managers may deploy the savings of individuals seeking long-term protection of their personal retirement capital for objectives partly determined by the state. It is unknown to what extent contributors are informed about these purposes and associated risks. Should there be full disclosure there is a possibility that government employees may raise the power and urgency of the contributors’ ‘voice’. They can even become ‘dangerous’ in their demands for access to or influence over the decision-making process.

Institutional investors … may also obstruct decision-making through ‘non-decisions’.

It is a question of time. In all the participant discussions on the factors influencing the investment decision-making process toward RI, time was a common denominator. Time was a factor in investment decisions, disclosure, communication and cost. Time was associated with the scheduling, frequency and length of meetings for all constituents involved in the investment decision-making process. Time was mentioned as a key determinant for assessing investment and investor performance. Time was a fundamental input into the calculation of fund liability in actuarial models. Time defined the thresholds of the materialisation of financial and ESG risk impacting both current and future generations. Time therefore needs to be integrated in all dimensions of the framework.

Stakeholder interests through the value chain are not aligned. Private sector asset managers and professional service providers were all profit-driven organisations, employing expensive professionals supported by costly infrastructure to deliver services to clients. Private and public-sector asset managers were fee-conscious custodians of contributor capital, governed by trustees who accepted the liability of their position, while typically receiving no additional remuneration for their services. Asset owners seek returns from their assets to meet liabilities of a legal entity that is, by definition, a not-for-profit organisation. Asset owners accepted the fiduciary duty for the funds over which they preside, but were the least familiar with the complexity of investment decision-making and responsible investment. Professional service providers and asset managers accepted the responsibility for most of the investment decision-making process for a fee but were unaware of the contingent liabilities attached to the services they provide the public. This highlights the need for ongoing training in this regard.

The future of responsible investing in South Africa

This study explored the factors influencing the institutional investor decision-making process towards responsible investment in South Africa. In particular, the research focused on understanding the connections, or lack thereof, between the decision-makers responsible for allocating the capital and the impact of those decisions on the stakeholders in the investment value chain.

Of concern is the small percentage of institutional investors who are signatories of the PRI relative to the number of stakeholders in the South African institutional investment community. Participant feedback suggested that the value proposition offered by the PRI to local institutional investors, versus the cost, does not appeal to smaller institutions. What is even more worrying is evidence of limited commitment from PRI and CRISA supporters. Shareholder activism in South Africa, until recently, has been relatively muted. With the all the scandals and controversies around executive remuneration, governance failures and other ESG risks, public shareholder engagement will in all likelihood grow in future.

The integration of ESG considerations demand that decision-makers accept complexity. Institutional investors are ultimately responsible to mediate between the interests of the profit-driven companies for which they work, while optimising the savings funds dutifully provided by other stakeholders who place their assets under their care.

Responsible investment provides institutional investors with an opportunity to play a transformative role in addressing some of the challenges that South Africa is facing. Through the integration of the PRI and CRISA, with a stakeholder stewardship-oriented approach, institutional investment decision-makers can indeed provide voice and access to the decision-making process for marginalised stakeholders. This more inclusive approach creates greater accountability in the investment system and encourages stakeholder participation.

Based on the study’s findings, the researcher made various recommendations to stakeholders in ecosystem of institutional investors. Here are some of these recommendations:

Incentive systems have the power to reinforce behaviour. Investment incentives are often driven by short-term horizons, despite the underlying premise of RI seeking sustainable returns over longer-term horizons.

Recommendations to asset owners

- Improve the engagement of asset owners with assets, contributors and beneficiaries: Evidence suggests a disconnection between local asset owners and other stakeholders in the investment value chain. Improving asset owner engagement with the directors and management of investee companies in the commercial dimension, and contributors and beneficiaries in the contractual dimension, will help to address this disconnection. In light of the societal impact of pension funds on investment and provision for future generations, it is recommended that the costs of trustee training be recovered from the state via the financial regulator.

- Review the governance structures of pension funds: Asset owner governing bodies or boards of directors should review the structures of pension fund governance to ensure alignment with King IV recommendations. This would likely affect the way in which the individuals are selected to serve on such boards. Participant feedback confirmed that there is a lack of additional remuneration for attending to trustee duties. In addition, the lack of parity between employer and employee representatives could be intentionally overlooked. Similarly, information asymmetry between the contributors and institutional investors may be orchestrated by both employers and skilled employee representatives to protect one set of interests over another. To support independent decision-making, it is recommended that an independent, skilled and non-executive chairperson be appointed to mediate the interests of the trustees. It is also proposed that additional professional trustees be recruited where there may be a lack of parity in terms of financial literacy, or a lack of independence due to employer or employee interests. In addition, financial and administrative literacy should be significantly improved for inclusive decision-making.

- Delegate fewer duties and manage conflicts of interest: The enormous responsibilities that asset owners delegate to asset managers and professional service providers is a concern as it can disempower the governing body and raise the potential for conflicts of interest. In principle, asset consultants might fulfil this role, but a clear separation between the interests of professional service providers, asset managers and asset owners is recommended. As the interviewees pointed out, asset managers and professional service providers play many roles in the investment system, serving many masters.

- Shift the decision-making horizon: The researcher found that funds usually have a longer investment horizon (20 years or more) than institutional investors (typically between five and 10 years). The researcher recommends that asset owners implement investment decision-making processes that consider long-term scenarios. The following should also be considered: future generations, multiple time horizons, saving, ongoing financial literacy education, and stakeholder participation in the investment decision-making process. Also, mandates could be shared with contributors and beneficiaries to enhance decision-making transparency.

RI is not a fund or a signature, it’s an investment philosophy.

- Build the reputation of asset managers: The study participants said the success of asset managers depends on their ability to maintain their reputation and deliver returns. Reputation in this context is underpinned by professional service, acquiring and retaining clients, and consistent investment performance.

- Turn RI practice into opportunities for growth for asset managers: The researcher believes that responsible investment brings additional layers of service to asset managers’ value proposition, which can enhance their reputation. However, some institutional investors see this as unnecessary and an additional cost. Firstly, responsible investment and integrated reporting are increasingly being required by industry bodies. Secondly, the reconfiguration of asset manager evaluation criteria towards more RI-orientated metrics might shift how asset owners and professional service providers ascribe value to and remunerate asset managers. From a reputation perspective, asset managers could assume wider responsibility and start to educate their clients about the potential financial implications, as well as ESG impacts, of their choices. The researcher recommends that institutional investors actively engage with the PRI community and leverage the value it offers to signatories.

- Restructure the remuneration of asset managers: Asset managers’ remuneration should not be linked to investment performance alone; a fee-for-service based approach is also suggested. By adopting responsible investment as an embedded philosophy, asset managers assume responsibility for active ownership, communication, ESG risk identification, monitoring and reporting services that could build their revenue pipeline away from cost structures based on assets under management. This approach could protect clients’ interests and enhance the reputation of asset managers and service providers.

- Mandate compliance: The PRI’s increased power as a stakeholder could be leveraged through research and case studies confirming the value of RI. The benefits for asset owners to recognise asset managers and professional service providers for incorporating the philosophy of responsible investment into mandates could be highlighted through such case studies.

Reputation, not just performance, influences investor practice.

Stepping up efforts to integrate responsible investment

Institutional investors, in concert with the state, play a pivotal role in the global financial system. As the custodians of other people’s money, they are responsible for delivering on the long-term financial objectives and needs of the contributors and beneficiaries of those investments. In addition, they carry a fiduciary duty toward current and future generations.

Repeated examples show that sustainable, risk-adjusted returns are a function of collective stakeholder alignment throughout the investment value chain. The traction of frameworks – such as those proposed by King IV, PRI and CRISA – suggests greater responsibility is being taken. However, personal conviction by individual decision-makers is required to promote these principles with peers.

In South Africa and elsewhere the word, the prevailing level of income and wealth inequality between nations, institutions and individuals are wicked problems manifested through volatile financial, political and social movements. The demands for trade, employment and wage increases seemingly stand in tension with the competing needs for prioritising the environment, increased automation and maximising returns for shareholders. The balance between self-interest and collective progress is precarious.

Responsible investment can indeed become a dominant investment philosophy. This calls for commitment from the individual investment decision-makers and their institutions. It also calls for proactive communication, education and engagement by all the participants in the investment decision-making process.

- Dr Colin Habberton is a PhD alumnus of the University of Stellenbosch Business School. The title of his PhD dissertation is: Connecting capital: The factors influencing the decision-making process of institutional investors towards responsible investing. Find his thesis here: http://scholar.sun.ac.za/handle/10019.1/105695

- The supervisors for his PhD dissertation were Prof Suzette Viviers and Dr Lara Skelly.