Is FinTech the fix for financial inclusion in Africa?

Around the world, financial inclusion strategies and principles are directly linked to economic growth and employment statistics.

About financial services, growth, and technology for all

Around the world, financial inclusion strategies and principles are directly linked to economic growth and employment statistics.

Not all financial inclusion initiatives have worked so far. There are cases where financial inclusion initiatives have failed even though similar measures were introduced in the different territories. A generalised model can therefore not be used to meet financial inclusion targets because success depends on the idiosyncrasies of each country.

Around the world, financial inclusion strategies and principles are directly linked to economic growth and employment statistics.

In this context, it is also essential to understand the financial inclusion landscape, which is characterised by:

- The ongoing evolution in the financial industry

- Exponential advances in internet-based technologies

- Lower entry barriers to the financial industry

- Diminished or poorly defined boundaries in some financial services’ eco-systems.

In the past, the financial services industry was dominated by banks, insurers and investment houses. Now technology companies are also making their mark in this landscape. What’s more, the splicing of finance and technology, known as FinTech, is broadening the financial industry. While new competitors in the market might impact adversely on traditional banks, FinTech could be a powerful tool to create financially inclusive societies.

The growing importance of financial inclusion

Complete financial inclusion is a state in which all people have convenient access to a full suite of quality financial services at affordable prices. Financial inclusion allows access to a wide variety of products and services to ensure positive outcomes for individuals, households, micro and macro enterprises, and regional economies.

Although the concept of financial inclusion has been topical for several decades, global financial inclusion only recently became essential political and strategic building blocks in most countries.

A surge of findings over the past decade made it clear that financial inclusion is not just an emerging markets issue. It also affects advanced economies. Even in developed countries, large segments of global populations still do not have bank accounts. In fact, in 2015, around 2 billion individuals in developed countries still did not have their own bank accounts. These people are financially excluded from economic resources, access to basic services, property ownership, inheritance, natural resources, appropriate new technology, financial services and microfinance.

Financial inclusion can help to alleviate poverty and stimulate economic growth. It can help to eradicate famine, support health and well-being, ensure quality education, resolve gender inequality, safeguard pure water supplies, provide hygienic sanitation, supply affordable and clean energy, create employment opportunities, inspire innovation, secure infrastructure, and generate justice and peace for all.

Technologies at work or not at work

History is littered with cautionary tales involving adoption rates and the applicability of new technologies. New technology does not necessarily lead to acceptance and mass implementation. In fact, mass acceptance depends on the technology itself and the way in which stakeholders perceive its added value.

For example, in 2001, Segways scooters were heralded as the future of individual transportation. It was thought that these new self-balancing, two-wheeled personal transport devices would change the way humanity thinks about personal transportation. It is now almost two decades later, with the original scooters still going strong while the uptake of Segways remains limited.

However, other technologies have massively altered human behaviour. In just over a decade, in June 2016, Facebook exceeded all expectations and acquired 1.71 billion globally active monthly users.

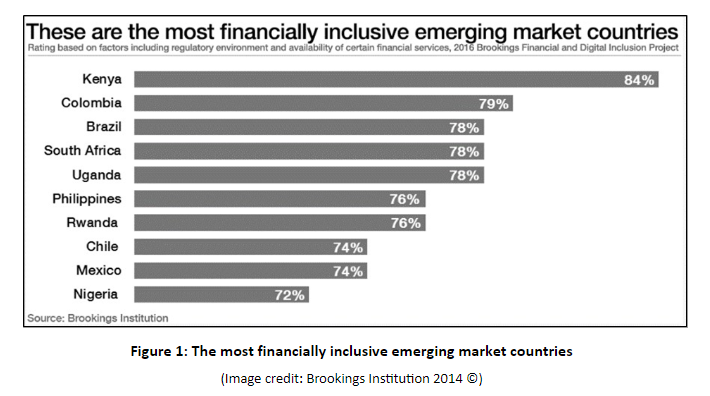

The financial services industry also has evidence of mass adoption rates. M-Pesa, the mobile money provider in Kenya, is part and parcel of the Kenyan economy. In 2013, the M-Pesa user base of more than 18 million illustrated the significant social and economic impact of technological innovation. Kenya is the most financially inclusive emerging market economy, with South Africa in the overall global fourth position, and in second place on the African continent (see Figure 1 below). Yet, the uptake of the M-Pesa failed in South Africa. It was launched in the country in 2010 and shut down in July 2016.

These contrasting outcomes of the same technology-based solutions is a stark reminder that technology itself is not a panacea. Various underlying variables lead to success or failure.

FinTech provides a powerful, readily available and effective mechanism to help eradicate poverty and achieve global financial inclusion.

Enter FinTech

FinTech is a combination of the words financial and technology, and the latest portmanteau to grace the covers of leading business and technology publications. The concept of technology in the finance world has been around for decades, but exponential advances and lower entry barriers are increasing the rate at which technology is being used to provide global financial services and products. So, FinTech is a moniker for the combination of technology and any area remotely related to finance. Its scope has gone beyond its origins of bank transactions and into adjacent areas such as insurance, lending, investments, digital crypto-currencies and personal digital identity.

Can FinTech help to facilitate financial inclusion?

This study investigated the barriers to a financially inclusive society and wanted to find out if financial technology could be used as a mechanism to address financial exclusion on the African continent. The objective of the research was to postulate on various outcomes of a technological approach to solve the lack of financial inclusion in Africa and to understand which characteristics will ensure the use of sustainable financial technology over the long term.

Four distinct yet interrelated variables were identified:

- Providers: These are the institutions providing financial services and products.

- Products and services: These are the financial products and services offered by institutions, and products and services needed by consumers.

- Channel: This refers to the mechanism or conduit distributing products and services to consumers, or the method through which consumers prefer access to financial products and services.

- Consumers: These are the end users who benefit from access to and the usage of products and services.

The research design used a scenario approach. Scenarios are used to influence decisions by illustrating the consequences of those decisions over time. The scenarios weave together different concepts enabling participants to gain a better understanding of the building blocks, their interaction and the eventual outcomes. Scenarios are therefore ideal to illustrate the impact of choices, decisions, events and consequences.

The scenario field consisted of two areas, namely financial inclusion and FinTech. The variables associated with these two areas were identified. The purpose was to measure the impact of the variables on the rate of financial inclusion across the African continent.

Affordability for consumers … includes access to more funds, personalised interest rates and lower administration costs.

The four research scenarios and their nutshell explanations

- The Usual Exclusion Scenario: This is the reference scenario. The status quo remains intact and no change is implemented nor expected. Traditional providers are burdened by systems and processes which affect their ability to provide consumers with an appropriate range of products and services through suitable channels. FinTech providers are acknowledged but remain a systemic externality.

- Potentially Eventually Scenario: FinTech is hailed as a mechanism to facilitate financial inclusion. Traditional providers pivot parts of their business to create financial inclusion. Multi-national providers cross-subsidise consumer segments and geographical territories. These principles are combined with incentives to increase the reach of financial products and services. Non-traditional enterprises partner with traditional financial service providers to amplify market presence and log consumer data.

- Fast For a Few Scenario: FinTech technology is applied and rapidly accepted in geographical areas. Providers who deploy products and services to consumers in order to create a more inclusive society become a dominant consumer force.

- Africa Incorporated Scenario: Collaboration between various stakeholders ensures increasing financial inclusion for the excluded population. FinTech providers can innovate as long as they adhere to LASIC principles (Low margin, Asset light, Scalable, Innovative and Compliance easy).

Heed was given to these thematic barriers to entry:

- Affordability for consumers: This includes access to more funds, personalised interest rates and lower administration costs.

- Affordability for providers: This includes access to consumer data and profiles to offer appropriate products and services, the availability of products and services without expenditure on business premises, and products and services pinned at attractive price points.

- Access for consumers: This includes the availability of financial services in consumers’ immediate location, increased mobile penetration rates, access to bank transactions and a broad range of products and services, pay-point technology and connectivity reducing the need for cash in hand, and government authorities paying citizens electronically.

- Access for providers: FinTech can eliminate the need to build or run a business in areas with questionable economic viability. In addition, FinTech can leverage access points and increase product distribution without additional capital investment.

- Regulatory requirements for consumers: Documentation is reduced because government and financial service providers share data. Also, transactional records of financial services and products allow consumers to capitalise on credit with personalised interest rates.

- Regulatory requirements for providers: Consumer data allows providers to offer accurate price points and share risk. Also, government incentives and reduced compliance burdens encourage providers to offer financial services and products. The sharing of client data between providers lead to lower initiation costs and higher consumer acquisition rates.

- Financial education and literacy for consumers: National government, traditional and FinTech providers as well as third-party agents network and use campaigns to educate consumers about the value of formal financial services and products. Consumers learn about the correct usage of credit and how different ancillary financial services or products work so that they can take control of their financial journey.

Financial education and literacy for providers: Providers are usually faced with time-consuming education processes and little revenue during the process. Incentives are provided to third-party banking agents to educate consumers in order to compensate for the lack of revenue. Government supports initiatives and manages stakeholder expectations and responsibilities.

If FinTech is applied correctly, it could address provider and consumer concerns about affordability, access, regulation and financial education.

What does the future hold for FinTech?

Financial exclusion is a result of barriers limiting consumers’ access to financial products and services, and barriers limiting the ability of providers to supply products and services. Financial inclusion is a systemic problem requiring collaboration from multiple stakeholders to gain the expansion of financial inclusion and nurture continental growth.

FinTech provides a powerful, readily available and effective mechanism to help eradicate poverty and achieve global financial inclusion. It provides an opportunity which could contribute significantly to create a continent where most individuals are financially included. If FinTech is applied correctly, it could address provider and consumer concerns about affordability, access, regulation and financial education.

- Original research: De Bruin, S.J. 2017. Scenarios for the excluded: A technological approach to financial inclusion in Africa. Unpublished MPhil in Futures Studies research report. Bellville: University of Stellenbosch Business School.

Stephanus J de Bruin completed his research report under the supervision of Prof André Roux as part of his MPhil in Futures Studies at the University of Stellenbosch. Prof Roux is the head of USB’s Futures Studies programmes.